Legal Strategies to Reduce Corporate Taxes

페이지 정보

본문

Corporate taxes often weigh heavily on firms, especially those situated in high‑tax regions or running on thin margins.

Even though loopholes and aggressive shelters lure many, the safest and most enduring route is to employ legitimate, legal methods that lower taxable income, boost deductions, and capitalize on available credits.

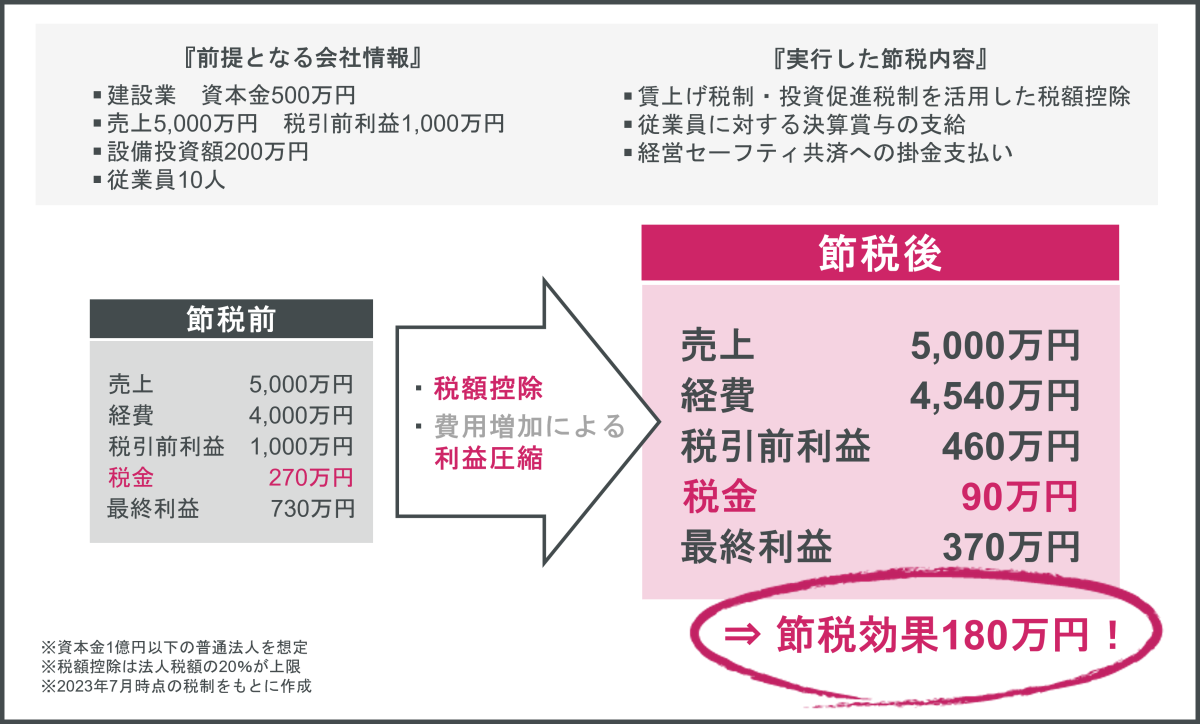

Here are practical, 中小企業経営強化税制 商品 compliant methods to reduce corporate taxes without straying from legal boundaries.

1. Reconsider Your Corporate Structure

Choosing the right legal entity can have a big impact on tax liability.

C‑Corporations vs. S‑Corporations: In the U.S., an S‑corporation forwards income, deductions, and credits to shareholders, sidestepping double taxation.

If your company qualifies, moving from a C‑corporation to an S‑corporation can remove corporate‑level tax entirely.

Limited Liability Companies (LLCs): An LLC has the option to be taxed as a partnership, S‑corporation, or C‑corporation.

Choosing the most favorable election can lower the total tax load.

Holding Companies: Creating a holding entity that owns subsidiaries can provide dividend tax benefits, particularly if the holding company resides in a low‑tax jurisdiction while complying with international rules.

2. Increase Deductible Business Expenditures

Every lawful business cost cuts taxable income.

Operating Costs: Rent, utilities, wages, marketing, and equipment purchases are fully deductible.

Depreciation: Use accelerated depreciation schedules (e.g., Section 179 in the U.S.) to write off the cost of property and equipment in the year it is placed into service.

Research & Development (R&D): Numerous jurisdictions provide sizable R&D tax credits for eligible research work.

Invest in new product development or process improvements to qualify.

Travel & Entertainment: After recent tax law revisions, confirm that meals and entertainment costs satisfy stricter constraints and retain detailed records to justify any deduction.

3. Take Advantage of Tax Credits

Unlike deductions, credits reduce tax liability dollar‑for‑dollar.

Energy Efficiency Credit: Adding solar panels, wind turbines, or other green energy systems can earn substantial credits.

Workforce Development Credit: Recruiting particular employee categories (e.g., veterans, residents of low‑income communities) may earn tax incentives.

Foreign‑Earned Income Exclusion: Operating abroad may allow you to exclude part of foreign income under certain conditions.

State‑Specific Credits: Several states or provinces grant credits for job creation, regional investment, or community initiatives.

4. Schedule Income and Expenses

Proper timing can move income into a lower‑tax year.

Deferred Income: Push invoices into the next fiscal year if you foresee a lower tax bracket.

Prepaid Expenses: Settle upcoming costs before year‑end to front‑load the deduction.

Capital Gains vs. Ordinary Income: If you have significant capital gains, consider harvesting tax losses through a wash sale strategy (where allowed) or postponing asset sales.

5. Leverage International Tax Planning

Operating worldwide unlocks further opportunities.

Double Taxation Treaties: Apply treaties to lower withholding taxes on cross‑border payments.

Transfer Pricing Compliance: Ensure that intercompany charges reflect arm‑length pricing to avoid penalties and re‑assessment.

Foreign Tax Credits: Redeem credits for overseas taxes to offset domestic tax.

Low‑Tax Jurisdictions: Provided you adhere to the law, you can establish a subsidiary in a low‑tax area (e.g., Ireland, Singapore) if it matches your operational needs and compliance obligations.

6. Apply Tax‑Efficient Financing

How you finance operations can affect taxes.

Interest vs. Dividends: Interest on debt is deductible, but dividends are not.

Employing debt financing (while keeping a sound debt‑to‑equity ratio) can cut taxable income.

Lease vs. Purchase: Leasing equipment often provides a deductible cost each month, while purchasing may offer depreciation.

Evaluate the overall tax effect across the asset’s lifespan.

Employee Stock Options: Offering stock options can defer compensation costs until the options are exercised — and align with a lower tax year.

7. Keep Solid Documentation and Compliance

Even the best‑designed tax strategy can falter if documentation is lacking.

Detailed Records: Maintain receipts, contracts, and justifications for every deduction or credit claim.

Audit Plans: Examine and refresh audit procedures yearly to withstand a tax audit.

Professional Guidance: Partner with a tax advisor versed in domestic and international law to keep abreast of changes and new opportunities.

8. Ongoing Review and Adaptation

Tax statutes change, and business realities shift.

Annual Tax Strategy Meetings: Review your tax position each year with your CFO and tax advisor.

Scenario Planning: Forecast how variations in income, expenses, or rules could influence tax liability.

Stay Informed: Subscribe to tax newsletters and attend industry conferences to learn about new incentives and legislative changes.

Summary

Lowering corporate taxes is not about finding loopholes—it’s about making smart, compliant choices that reduce taxable income and take advantage of legitimate incentives.

Through careful entity structuring, maximizing deductions and credits, timing income, and thoughtful international planning, you can build a tax strategy that fuels growth while honoring the law.

Regularly review your approach, maintain meticulous records, and consult qualified professionals to ensure that your tax savings are both effective and sustainable.

- 이전글비아그라연예인 비아그라복제약 25.09.12

- 다음글The Evolution of Mobile Casino Gaming 25.09.12

댓글목록

등록된 댓글이 없습니다.